The Tinman's Time has Come? Exploring Tin and Alphamin

The Tinman's Time has Come? Exploring Tin and Alphamin

A detailed look on how current unrest in Myanmar is affecting the supply chain for tin and how Alphamin Resources is best positioned to capitalize.

As the current unrest in Myanmar has escalated due to its ongoing initially peaceful, yet now violent, coup d’etat; the world has watched closely. Initially peaceful towards protestors, the military has escalated the conflict to become extremely violent, leading to nearly 114 protestors being shot, seven of the victims children. The international community has scorned these continued acts of violence towards Myanmar’s own citizens, and are observing the military’s continued actions closely. Yet, in nearby China, economists are closely watching another part of Myanmar: the tin ore mines in the mining hub of Monywa, which China relies on for much of its Tin imports.

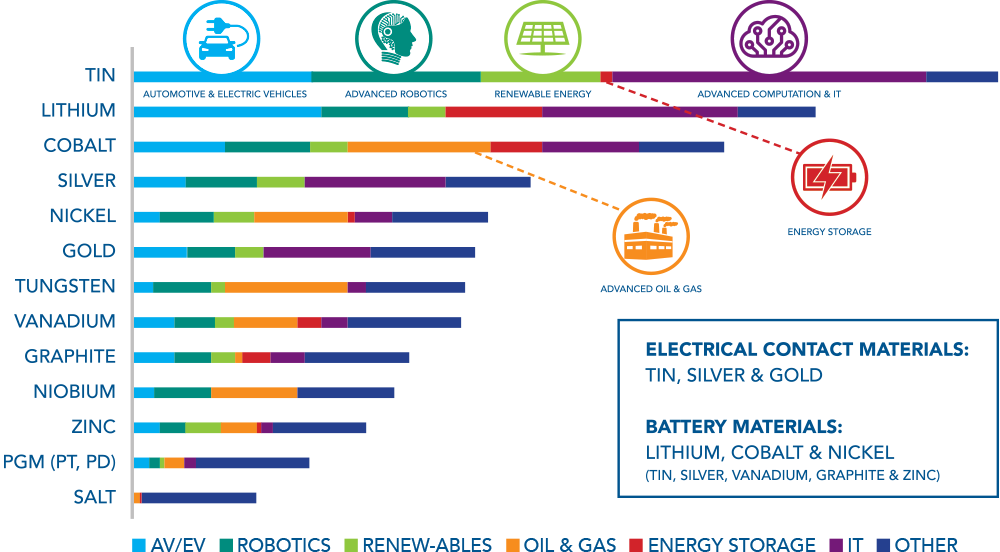

Before we delve into why tin ores and concentrates are so important to China, let’s first overview exactly what the uses of tin are.

Tin Uses

Tin is a metal often referred to as “The metal with which the Fourth Industrial Revolution will be built”. Researchers predict that tin will be the material of choice for future innovations in energy generating, storage, and advanced computation devices.

Below is an overview of the five largest applications for tin according to the International Tin Association, or ITA.

Tin Chemicals

Tinplate

Copper Alloys & Manufacturing Processes

Lead-Acid Batteries

Solders

Although each area listed above has its own importance to the global economy, for the purpose of this write-up I will specifically highlight the role tin plays in lead-acid batteries and solders.

In lead acid batteries, metallic positive and negative grids are formed into plates, which help initiate a chemical reaction from lead metal to lead sulphate; leading to this reaction discharging energy. Multiplied over many concurrent plates in series, there is a large amount of voltage output that can provide affordable power as a result of the cheap pricing of lead-acid batteries compared to lithium-ion. Battery plates vary in size based on their application. The addition of incorporating tin as an alloy to said plates is a practice that enhances the capabilities of lead-acid batteries. The ALABC published a study in 1995 that concluded that adding tin and silver can increase up to 5% performance output of lead-acid batteries for electric vehicles, increasing cycling performance, reduced corrosion, and improved heat resistance.1

Solders is a metal alloy made with some form of a mixture of tin and lead used in the fusing of different types of metals. Specifically, solder is predominantly used in the joining of metals on electronics devices, such as semiconductors, computer circuitry, microcontrollers, and more. As a result of continued innovations in electronics and a need for increases in performance and reliability, previously majority lead solders have been phased out for tin based solder. In 2015, the ITA put out a report noting how increased miniaturization, complexity, optimization, and processes will be driving factors in innovating existing soldering technology and materials with new, lead-free technology; mainly using tin. The lightweight of tin alloys compared to lead alloys decreases the risk for weight loads negatively affecting densely packed circuit boards, among other benefits.2 Fast forward to 2021, semiconductors are a scarce commodity due to supply chain constraints, and tin plays a large role in the ability to implement said semiconductors into electronics boards.

China and Tin

Now, back to why China cares about having consistent tin imports:

Although lithium-ion batteries dominate the production lines of Chinese battery manufacturers, lead-acid batteries are still in heavy production in China due to their cheap cost. The production of said batteries demand ample tin concentrate reserves to produce effective devices for cheaper priced combustion engines. Nonetheless, poor practices in lead-acid battery production and recycling in China has lead to a hypothesized link between environmental and human lead positioning in China; leading to a mass crackdown of lead-acid battery production facilities being closed in May of 2011 for safety checks, to ensure lead was not polluting ecosystems and local drinking sources.3 Lithium-Ion batteries will continue to outpace production of lead-acid batteries for EV’s in the future, indicating though lead-acid still demands tin ore for production, it is not the predominant driver of tin imports.

That driver is solder. Soldering accounted for 48% of global usage of tin in 2018, and will continue to grow as the need for semiconductors grows; specifically in China.4 In 2020, China made less than 6% of the total number of chips that it used, yet it aims to grow this number rapidly; with a target of 70% of all chips it uses being made domestically by 2025, a lofty target.5 Tin is the glue (literally) that binds much of the chips needed for all electronics today and for China to reach its lofty target of 70% by 2025, it will need ample tin for soldering. China has long been the largest market for solder and will continue to be for many years with movement away from lead alloys in solder (a result of the previously mentioned effects of reckless lead-acid battery production) to predominantly tin and silver based alloys.

So, China needs lots of tin to ensure it has lots of semiconductors by 2025, where is it going to get that?

Well previously the answer has been from Myanmar. In 2015, the discovery of a new mysteriously discovered mine in the country’s Wa region led to high grade ore flooding the market and dropping tin prices globally. The mines helped supply 30% of Chinas demand for tin and 10% of demand worldwide, growing to 95% of China’s imports of tin ore in 2020.6 China does have domestic tin ore mines in the South China region, but they do not produce enough ore to fully prevent the need for ore imports.7

But with the tin supply coming under pressure due to a mixture of the ongoing coup, heavier-than-normal seasonal rains, and some environmental inspections, some small and medium-sized tin smelters in China are slated to halt production in April.8 This supply chain shake up is leaving the Asian behemoth to search to diversify its sources of tin ore and concentrate; no easy task for a country that houses three of the top five largest producers of refined tin.9

So, where are they going to get more tin from? The answer may lie in the heart of

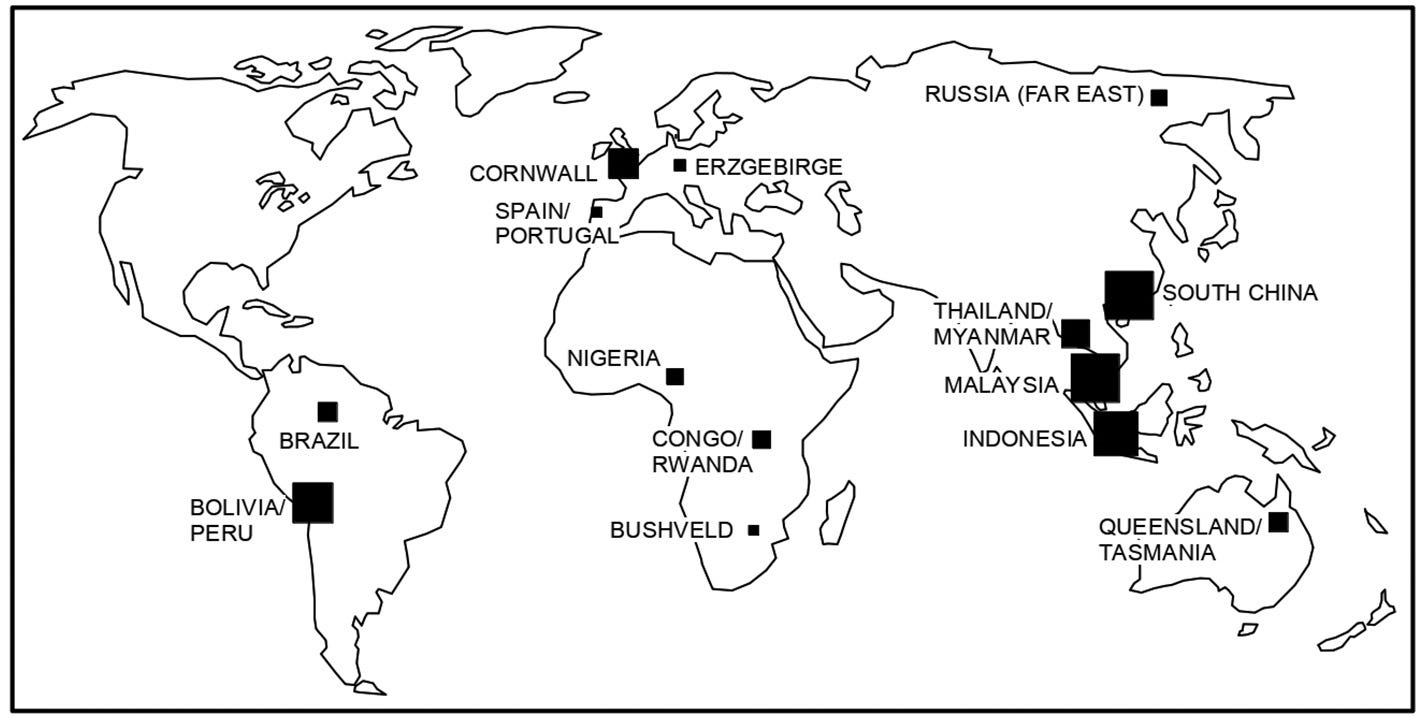

The Global Tin Mining Landscape

Roughly 85% of all mined tin is from a select few tin ore provinces: Southeast Asia (40-45%), South China (20%), Central Andes (14%), and Cornwall, UK (7%).

Interestingly enough, small-scale mining is a unique feature to the tin mining industry, and these small mines contribute 40% of the global market as of 2014.10 A contributing factor to this is the fact that many artisanal tin mines rarely define or report resource outputs.

Not all ore is the same; the grade of the ore is an indication of the concentration of the tin ore it contains. The higher a grade, the higher the output of tin a refiner can reach from a set amount of ore, and the more valuable said ore is. Grade is traditionally calculated through the following equation:

(amount of tin metal / amount of ore rock) * 100 = Grade % 11

There are many mining companies mining tin ore globally, but few have a combination of mining supply capability and high grade tin ore. In the North Kivu Province of the Democratic Republic of Congo, or DRC, high grade tin was discovered and the Bisie tin project was born as a result. The tin from the Bisie tin underground project was discovered to yield the worlds highest grade tin, at roughly 4.5%; nearly four times higher than most other tin mines in the world. Production on the mine has only recently completed, with initial construction starting in 2017 and finalizing in early 2019. The completed construction was only for phase 1 of the project, which is focused on developing the Mpama North region which is projected to produce 9,900 tons of tin a year until 2027. Phase 2 and 3 will focus on developing the Mpama South and Deeps regions, respectively.12

The high grade of ore and notable size of the mining project is what makes this mine in the DRC such an intriguing opportunity for tin investors.

Alphamin Resources: AFMJF

Overview

The majority stakeholder in the Bisie tin underground project is Alphamin Resources (US:AFMJF), who holds 80.75% stake in the project while the DRC Government and Industrial Development corporation of South Africa hold minority stakes in the project.

Alphamin is led by Maritz Smith, Chief Executive Officer & Director of the company; a seasoned professional in the mining industry who previously held the positions of Finance Director of Pan African Resources Plc, Chief Financial Officer at Continental Coal Ltd. and Chief Financial Officer and Director at Metorex Ltd.

The Value Proposition of Alphamin is the following:

Exposure to Growing Tin Market

World-class Tin Producer

Exploration Activities on 13km strike at Mpama South deposit

Entrepreneurial Management and Strong Community Relations*

*Now what the leadership of Alphamin meant by this when they outlined it in their Q4 2020 Investor Presentation Meeting was that they have a good relationship with the DRC, as historically, political unrest has been one of the main risks to successful and predictable business revenue in Central Africa. A direct DRC stake in the mine coupled with outreach relations efforts from Alphamin has ensured strong regional as well as national support from the DRC and the surrounding communities, as continued returns to the DRC as well as job creation is dependent on consistent exports of tin ore. Alphamin is also a compliant conflict free tin producer, ensuring that the tin ore that is sourced is reliably and consciously sourced with fair labor practices. The company has also increased its community footprint by implementing beneficial social projects such as implementing potable water, developing micro-hybrid energy, and building local schools. Alphamin describes its relationship with the neighboring community as “symbiotic”.

The “Alpha” in Alphamin comes directly from the previously mentioned high quality of the tin ore that is mined. Not only that, but the Bisie tin underground project also has significantly lower costs than many global peers; with ASIC in the lowest quartile of major tin producers at USD 10,800/t, nearly 40% margin over recent tin prices.

Speaking of tin prices, there are numerous factors that support increased prices between low global interest rates, high demand for semiconductors and thus tin, as well as low global tin ore supply to meet global demand. Demand for tin is quite inelastic - regardless of price, tin will continue to be needed by major countries, such as China, to meet lofty semiconductor production targets. In fact, Alphamin projects that price will need to increase to incentivize more development of tin ore so as to not cause a deficit.13

Tin prices are already in the midst of a major ascension, with tin prices per kg increasing nearly 25% year-to-date:

Beyond the immediate tailwinds of increased demand for tin ore and increased tin prices, Alphamin has also put up some impressive numbers confirming their rapid growth over the first few years of mining activity at Bisie.

Financials

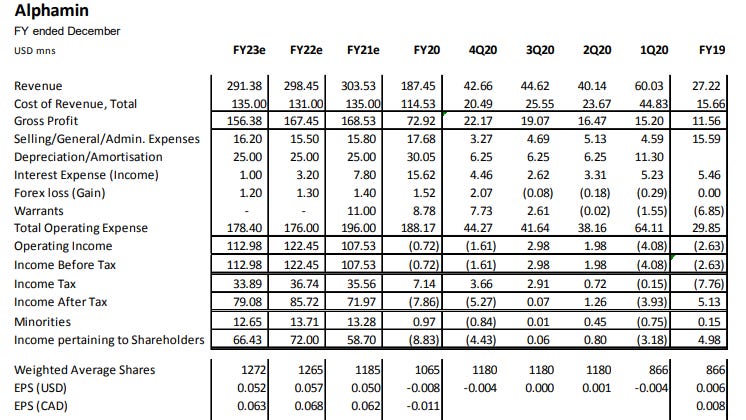

Revenues have increased at rapid pace, from 27.22m in FY19 to 187.45m in FY20, a CAGR of 162.42% over the two years of revenue generating operation at the mine. Operating income losses have decreased over the two years of operation and are projected to be net positive in FY21 based upon company estimates. FY21 is also projected to be a stand-out year in moving to positive EPS.14

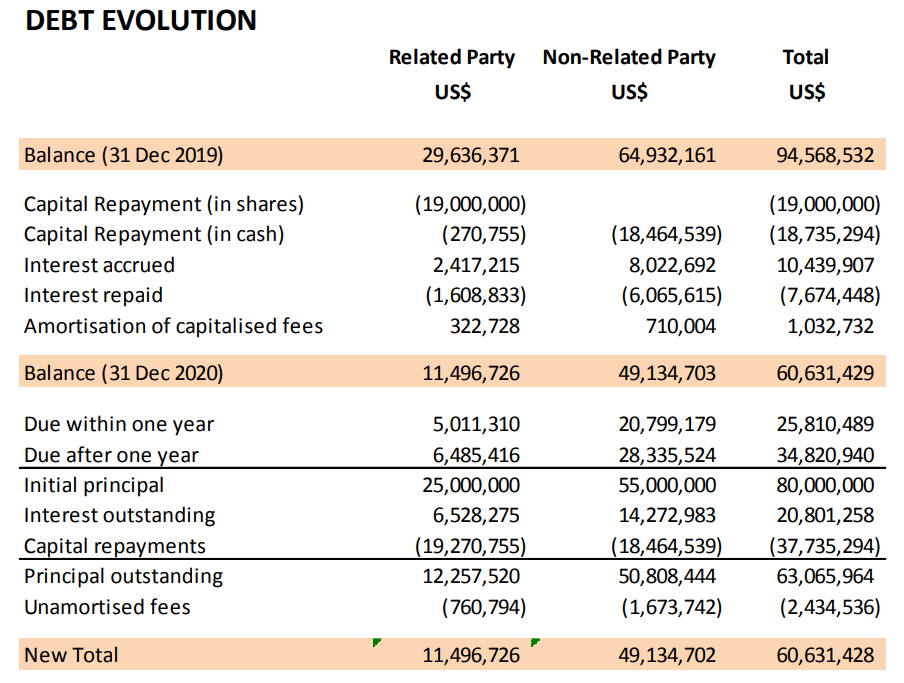

With any new developing mine, attaining the resources to build out production is cost intensive, and requires the accrual of debt.

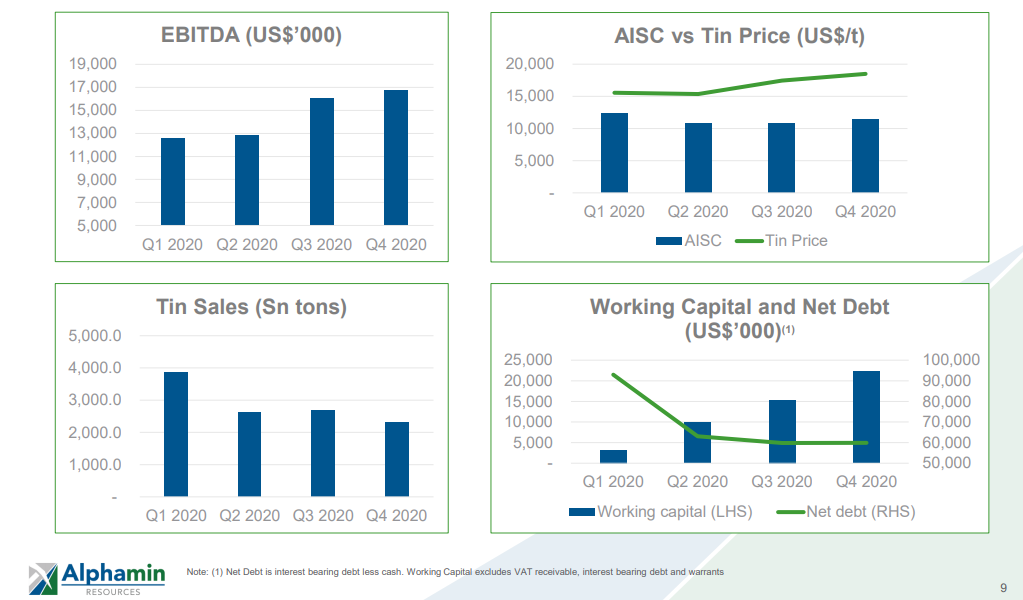

Quarter over quarter in 2020, Alphamin grew working capital while decreasing net debt by a large margin. EBITA increased into the latter half of 2020, while tin sales decreased from Q1 into Q4.

The company has done a good job in paying off roughly 1/3 of its outstanding debt balance from FY19 in 2020, and increased tin prices into late 2021 can pose another tailwind in allowing the company to use increased profits to pay off additional debt faster and potentially make a faster move towards being debt free than initially thought. As a part of the recent Q4 2020 earnings call, a dividend policy was mentioned to be considered by the Board towards the end of 2021. Existing FCF into 2021 will be focused on settling external debt as a priority. Current debt levels amount to less than a quarter of projected gross revenues for FY21.

Investor Interest

Increases in tin prices have increased investor attention, with recent coverage on the company initiated by Hallgarten & Company and Edison Group, both long on the tin miner.15

Currently price for AFMJF is not as liquid as major investors would hope, however with a US based listing, liquidity could be greatly increased and institutional attention would grow. Yet, trading volumes have still drastically increased over the past few months, from 6.3m shares in Dec. 20 to 31.4m shares in Feb. 21. Further increases in the price of tin may incentivize further investments in the tin mining space, similar to investments in gold and silver miners. This would also increase share trading volumes for Alphamin on a month-to-month basis.16

Risks

As previously mentioned, the primary risk to Alphamin’s mining operations is domestic instability in the DRC. Historically, the DRC has been faced with numerous instances of domestic conflicts between militant groups, kidnappings, and government battles. Although still affecting the nation, these acts of violence are still relatively scarce compared to the violence of years past.17 In addition, Alphamin’s network of security around the mine attempts to ensure that there are no disruptions to mine activities. Escalation of violence from militias or rogue guerilla factions is always a risk, however the DRC having a stake in the mine gives peace of mind any notable attack on the mine or it’s operations would be met with military support.

Compliance to Dodd-Frank is another lesser risk to Alphamin. Signed by President Obama in 2010, Dodd-Frank section (1502) requires companies who report to the SEC to disclose whether the previous metals used to make their products may have funded armed groups. The bill specifically references the area of concern to the the DRC, and implemented a de-facto embargo on metals from the area. This led to downstream companies avoiding purchasing from DRC miners for fear they would violate section 1502. In 2017, the SEC suspended enforcement of the rule referencing ‘conflict minerals’.18

Alphamin’s focus on providing fair labor tin ore is a byproduct of their focus on compliance of Frank-Dodd; and the clarity of their compliance actually aids as an advantage.

Lastly, the supply routes are an existing risk to the company’s operation of existing supply chains. In October 2019, a bridge on the primary transport route of the mine collapsed and resulted in supply chain delays while alternative paths were explored.19 The unfortunate event highlighted the need for multiple paths of transport for Alphamin and Bisie mine. Yet, the issue of weak and decaying infrastructure falls squarely on DRC itself, and is a symptom of a lesser developed economy with poor infrastructure. Alphamin can mitigate this risk by potentially investing in strengthening the infrastructure on these major routes as FCF increases over time.

Conclusion

More popular precious metals such as gold and silver have underperformed the market for the greater part of the past nine months. However, the mixture of scarcity of high grade tin ore/concentrates, ongoing supply shortage of semiconductors, and China’s desire to ramp up domestic production all make for compelling tailwinds for continued increases in the price of tin even in the midst of stagnant price action for precious metals. A more attractive investment than traditional commodity pricing is a high grade miner posting fantastic year-over-year growth numbers. Alphamin Resources is the tin miner that provides the best of both worlds, and should continue to increase growth as well as reduce debt to hopefully begin returning dividends to shareholders as soon as 2021. Soon it will be the tinman’s time to shine, he is getting more valuable by the day.

If you enjoyed this analysis, share and subscribe for weekly insights directly to your inbox below!

***This is not financial advice to buy or sell any security and leverd is not a financial advisor, please speak with your financial advisor if you have one.***

https://www.internationaltin.org/wp-content/uploads/2018/03/ITRI-Report-Tin-in-Lead-Acid-Batteries-260318.pdf

https://www.internationaltin.org/wp-content/uploads/2017/11/Solders-Technology-Roadmap-2015.pdf

https://ehjournal.biomedcentral.com/articles/10.1186/1476-069X-12-61

https://www.reuters.com/article/us-metals-tin-ahome-column/column-its-time-to-rethink-tin-the-forgotten-critical-mineral-andy-home-idUSKBN26Z25J

https://technode.com/2021/02/19/china-made-6-of-chips-it-used-in-2020-report/

https://www.ft.com/content/808c277a-6b53-11e6-a0b1-d87a9fea034f

https://www.internationaltin.org/mine-accident-further-tightens-chinese-tin-market/

https://www.internationaltin.org/china-smelters-halt-production/

https://investingnews.com/daily/resource-investing/industrial-metals-investing/tin-investing/a-snapshot-of-the-worlds-top-10-tin-producers/

https://www.sciencedirect.com/science/article/pii/S0024493720303935

https://undervaluedequity.com/mineral-deposit-value-how-to-calculate-the-potential-value-of-a-mining-project/

https://www.nsenergybusiness.com/projects/bisie-tin-project/

https://alphaminresources.com/wp-content/uploads/2021/03/Q4-2020-Investor-Presentation_Master.pdf

https://alphaminresources.com/wp-content/uploads/2021/03/ALPHA_FINANCIALS-2020YE.pdf

https://alphaminresources.com/wp-content/uploads/2021/04/Alphamin_April21_Update_2.pdf

https://alphaminresources.com/wp-content/uploads/2021/04/Alphamin_April21_Update_2.pdf

https://theconversation.com/violence-is-endemic-in-eastern-congo-what-drives-it-156039

https://www.internationaltin.org/dodd-frank/

https://roskill.com/news/tin-bridge-collapse-raises-uncertainty-over-alphamin-exports-from-bisie/

AFMJF owns 84.14% of the mine, after increasing its share in 2020