Is It Time to Re-evaluate China?

Is It Time to Re-evaluate China?

Loosened monetary policy by the Chinese Government and PBoC may begin to signal an encouraging environment for foreign investors in Chinese equities.

PBoC, or The People’s Bank of China, did something very peculiar a few weeks ago in late December; the bank lowered China’s one-year loan prime rate down 5 basis points to 3.8%.

Now although this may seem like a non-event, this was the first rate cut by PBoC since April 2020, when the full onset of the COVID-19 pandemic first hit the entire globe. The rate cut also comes during a very notable time of turmoil for the Chinese Real Estate market, the single largest market in the world in terms of specific sector. With the defaulting of Evergrande and current stress on the property market, the central bank knew that it was faced with an economic situation that needed to be accommodating - loosened rates to help encourage lending sure points to that.

Accommodating…

Across the globe in Washington D.C, the Federal Reserve released it’s most recent meeting minutes from its December meeting, which was anything but accommodative for markets. If anything, the meeting minutes emphasized a stark change of tone by many notoriously dovish Fed members, such as Neel Kashkari, who felt it would be best to prepare the markets for this hawkish tone by releasing a medium.com post about how runaway inflation could be a more persistent risk than previously thought.

Neel, btw deciding to release your thoughts on medium.com for the first time since Sept. of 2020 isn’t exactly the “stability” people want.

The Fed’s most recent minutes highlighted increased possibilities of a rate hike in March as well as three total rate hikes throughout 2022 and more aggressive runoff of the Fed’s balance sheet. All in all, not exactly the most attractive words to a market of investors with little options for return outside of equities and crypto.

The opposite of accommodating…

The massive bull rally we have seen since March 2020 haven’t come as a result of COVID, or tech growth, or any of those things (directly at least). The biggest reason for that injection of crack cocaine into the market was from a rapid move to nearly zero interest rates, and liquidity injections via Quantitative Easing, or QE (Fed bond buying).

You see where I am going with this by now hopefully. During a time where the Federal Reserve is working on tightening liquidity and raising interest rates, China’s economic environment is diverging, and they are looking to ease the current turmoil of the broken property market with lowered rates, and potential fiscal stimulus in 2022.

With that being said, it’s time we re-evaluate how we look at Chinese stocks.

Chinese Mega Cap Performance

China has notoriously cracked down the past year on many of its industries and companies that it views as out of line and in need of a firm hand from the government. After the fiasco of Ant Financials' botched IPO, where Jack Ma was viewed as skirting government rule in favor of international bragging rights, China cracked down heavy.

Tech leaders, including Ma, disappeared from the public; as billionaires turned from inspirations to public enemies. The government viewed it as an opportunity to focus more on the people as opposed to mega corporations. This ultimately led to many Chinese names being decimated in the markets in 2021:

BATX (Baidu, Alibaba, Tencent, Xiaomi) is to China what FAANG (Facebook, Apple, Amazon, Netflix, Google) is to US. These four stocks are usually viewed as mega cap tech names that have a great deal of international following and influence.

Since February 2021, all four of these names have been absolutely steamrolled due to both government crack down and international fears over delisting as US / China tensions have grown. The debacle with ridesharing app Didi’s IPO did not help at all either (man what a piece of shit that was).

Didi’s abysmal fall from grace put the nail in the coffin for many Chinese names, which continued their aggressive selloff as American and international investors divested.

But for the BATX names, this has resulted in what are now absurdly cheap valuations.

Baidu is currently trading at 4.46x EV/EBITDA, 16.45x Price/Cash Flow, and 7.16x Price/Earnings

Alibaba is currently trading at 11.35x EV/EBITDA, 17x Price/Cash Flow, and 17.03x Price/Earnings (with an Earnings Yield of 5.87%).

-To put this in perspective-

Nvidia is currently trading at 68.76x EV/EBITDA, 85.88x Price/Cash Flow, and 85.07 Price/Earnings. This is one of the most popularly held stocks currently as a result of the semiconductor mania…

I won’t compare Tencent and Xiaomi because they’re OTC on American markets, but I think you get the point right now. Chinese mega cap names are historically really cheap valuation wise. Biggest thing holding people back is a heavy handed government.

Government Inventive to Re-Strengthen The Private Sector

Look quite frankly, it’s not outlandish to say China has been experiencing a stealth recession.

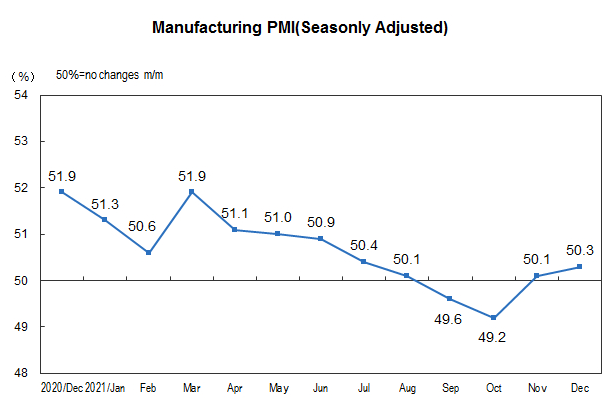

Manufacturing PMI decreased nearly every month of the year up until October:

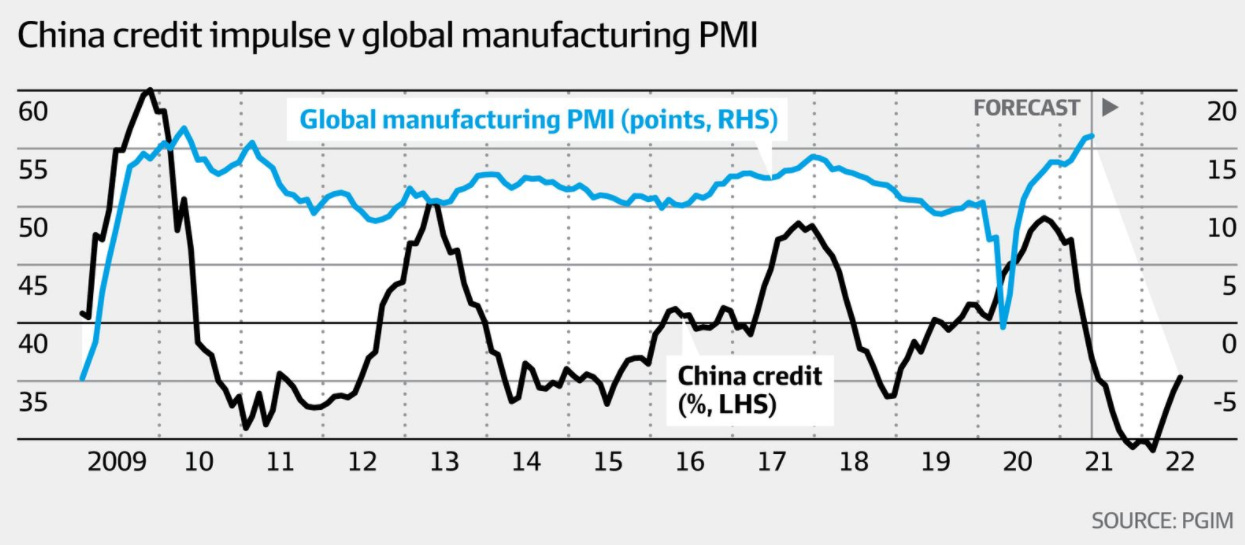

Credit Impulse vs Global Manufacturing PMI points to continuously decreasing credit until late in the year:

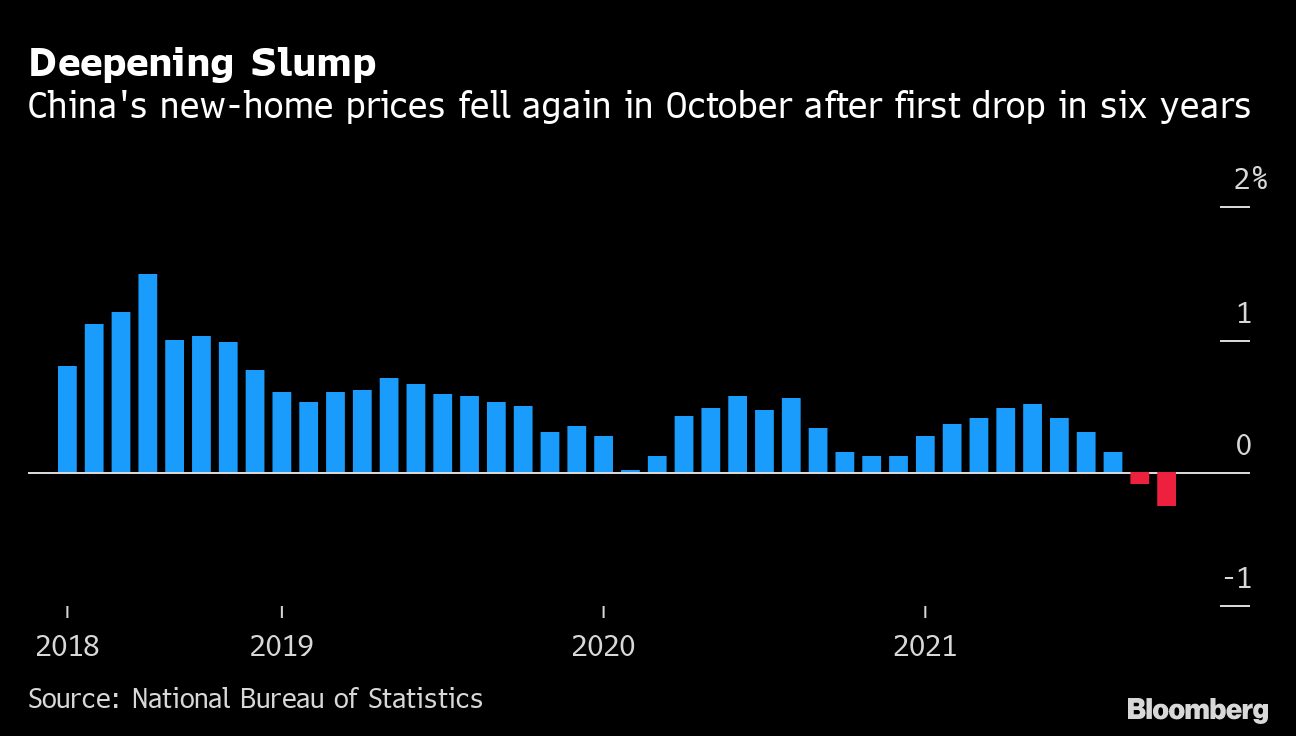

China Home Prices slump with more expecting lower prices in the future than higher prices for the first time in years:

This general slowdown has been greatly affected by China’s aforementioned dependence on real estate. Here is a crazy fact, nearly 70% of Chinese resident’s household wealth is in real estate, as opposed to that share being 35% in the US. Thus, the government has very large interest in keeping it that way.

When homebuilders begin to default after building new properties on credit, the following default hurts property prices and thus hurts money invested in real estate (again, a big chunk of the Chinese people’s money). Less desire to take out loans for new properties, equates in less liquid of a real estate market, leads to lowered prices, and the expectation of lowered prices in the future can lead to a mini death spiral for prices if PBoC doesn’t step in.

*exhale*

So… yeah they go and start lowering interest rates to help support it. But not only does this help spark liquidity in real estate, if only slightly, it attracts more foreign investors to Chinese assets in general as money is easier to obtain at a lower cost of carry.

So hawkish Federal Reserve + dovish PBoC + affordable Chinese mega cap names = Goldman Sachs crawling out of the woodwork in Shanghai.

Although that is a joke, it may not seem like it. Here is a recent blurb about Wall Street banks quietly deepening their Chinese ties this past year from Bloomberg:

“Some U.S. politicians have been calling for companies to back away from China, over concerns about national security and human rights. But Wall Street banks are instead deepening their ties. JPMorgan in August took full control of a securities joint venture with a Chinese company, and now wants to do the same with an asset management business it partly owns. Morgan Stanley is seeking five new banking licenses in mainland China in 2022, while Goldman Sachs Group Inc. has been doubling its workforce. Citigroup Inc. applied in December for a securities trading and investment banking permit and plans to seek a futures license in 2022, adding 100 employees in the country in all.”

But what about US regulators?

Perpetual Delisting Fears

Did you know that of the nearly 250 Chinese companies listed in the US, the majority are incorporated in the Cayman Islands? That includes behemoth Alibaba. Chinese companies use something called variable interest entities (VIEs) to skirt restrictions on foreign investments in tech, healthcare, and other industries.

Basically, these allow investors to exercise control via contractual agreements instead of voting rights. With this, Chinese owners can retain these voting rights over the original business, while the foreign shell company issues shares to foreign investors (ADR) and provides an investment vehicle in return.

As a part of China’s recent crackdown on foreign companies, the government wants to reign in these companies to begin to register under Chinese securities laws as opposed to being incorporated in the Cayman Islands. To me, it is less a move of restricting foreign investment in Chinese firms but moreso to reign in a lack of oversight that caused embarrassments like Didi knowingly IPO’ing with security issues from the Chinese government. Didi ironically also is incorporated in the Cayman Islands and not in China.

Didi’s delisting itself scared many, with many prominent investors predicting nearly all Chinese stocks will be delisted from US markets by 2024. There is a risk / reward ratio for everything in the stock market, and there is and in my opinion will continue to be an inherent risk to investing in Chinese names due to geopolitical issues with Taiwan as well as the SEC requiring Chinese firms to be subject to audits from the US; a practice Beijing does not allow.

At such low valuation multiples, the question to ask oneself is, what is the risk/reward now that some of these names are nearly 50% off their highs from last year.

Another prominent investor sees that r/r as favorable, this guy:

Yes, “this guy” is multi billionaire Charlie Munger, who announced he doubled his stake in Alibaba just this past week via Daily Journal Corp, a newspaper and software company owned by Munger. In Q4 the company indicated a new addition of 300,000 shares of Alibaba for a total of 602,000 shares.

“What you have to learn is to fold early when the odds are against you, or if you have a big edge, back it heavily because you don't get a big edge often. Opportunity comes, but it doesn't come often, so seize it when it does come.” - Munger

In the midst of an increasingly hawkish Federal Reserve here in the US that is poised to steadily suck liquidity out of markets to ease inflation pressures, PBoC’s policies are diverging in an effort to pour liquidity into their economy, little by little, to alleviate the stresses placed upon it by defaulting homebuilders such as Evergrande.

While US mega caps such as Apple hit unheard of 3 trillion dollar market cap valuations, Chinese mega caps sit idly at fire sale prices off of their recent valuations pre 2021. The phrase “the market is efficient” is one I hear often, but what most people don’t realize is that there is a point prior to one confidently boasting that when justifying a price move - where there is a value arbitrage opportunity.

Some understandably stay away from these high risk names, favoring the inflated valuation names that have carried them to high returns the past few years. Some leave equity markets altogether in hopes of less risky returns in fixed income assets. Yet amongst these crowds, some see the hand they are dealt as an edge to make a strategic risk/reward move, just as Charlie Munger would.

It is time to start reevaluating the cards on the table, and in this case, those cards are Chinese mega cap stocks.

Nothing in this post is to be constituted as financial advice nor a recommendation to buy or sell any equities or investment product, I am not a registered financial advisor. If making any investment decisions talk to a financial advisor first.